Download files

Complete book:

Individual page:

{kind=link}

Thumbnail gallery: Grid view | List view

62

STAMP DUTIES.

Personal property — Absolute power of disposal. —

Personal estate which a person, dying after 8rd April,

1860, shall have disposed of by will, under any

authority enabling such person to dispose of the

same as he shall think fit, shall be deemed personal

or movable estate of the person so dying, for the

purpose of payment of inventory, probate, or adminis-

tration duty.— (23 Vict. c. 15, § 4.)

Indian Promissory Notes — Ships. — Indian Gov-

ernment promissory notes and certificates issued, or

stock in lieu thereof, being assets of a deceased

person, the interest of which shall be payable in

London, registered in London, or enfaced in India

for the pn.pose of such registration before the death

of the owner; also Indian Government promissory

notes, with coupons attached, in the same circum-

stances as to registration, and certificates issued, or

stock created in lieu thereof, shall be personal estate,

and bona notabilia in England of the deceased person

(23 Vict. c. 5, § 1); also any sliip, or any share of

a ship, belonging to a deceased person registered in

any port in the United Kingdom, notwithstanding

such ship at the time of the death may have been at

sea, or elsewhere out of the United Kingdom, shall

be deemed to be at the port at which she may be

registered (27 and 28 Viet. c. 66), and liable to

inventory, probate, or administration duty.

Specialty Debts.— For probate and administration

duty, debts and sums of money due from persons in

the United Kingdom to a deceased on obligation or

other specialty, shall be estate and effects of the de-

ceased within the jurisdiction of Her Majesty's Court

of Probate in England or Ireland, in which the same

would be if they were debts upon simple contract,

without regard to the place where the obligation or

specialty shall be at the time of the death. — (25 Vict,

c. 22, § 39).

Foreign Bonds and Stochs. — Documents of the

debts of foreign governments and foreign companies

which pass from hand to hand are property where the

documents may be. Debentures or bonds by foreign

companies and governments, and the title to stocks

of foreign companies and governments, are property

in this country, if in the possession of any person in

this country, and can be sold in the market, and the

title of the purchasers completed to them in this

country. See Attorney-General v. Bouwens, 4 Meeson

and Welsby, 171

Companies under the Companies Acts whose objects

comprise business in a colony may have a branch

register of members resident in said colony. The

share of a deceased member registered in such colonial

register shall be part of the estate of such deceased

member for inventory duty, in like manner as if the

registration had been in the registered office of the

company, unless he shall have died elsewhere than in

the United Kingdom.— (46 and 47 Vict. c. 30, § 3

(7) (b), and 52 and 53 Vict. c. 42, § 18).

Rents of Heritage. — If the deceased survive Whit-

sunday, one moiety of the rents of the crop of that

year is personal estate. If he survive Martinmas, the

whole rents of that crop fall into the executry. In

addition, from and after 1st August, 1870, the Act

33 & 34 Vict. 1870, c. 35, would seem to give the

executor a proportion of the rents from the term pre-

ceding the date of death to the date of death. That

Act would also seem to give a proportion of the term's

rents of quarries, minerals, and houses, and also fen-

duties current at the death. The executor's right to

house-rents would not therefore be to the half year's

rents current at death, but to a proportion only to

the date of death.

Modes in which Dutt may be paid.

When deceased domiciled in Scotland. — In the

case of a person dying domiciled in Scotland, having

personal property in Scotland, England, and Ireland,

and also heritable securities excluding executors, and

personal bonds excluding executors, duty in respect

of the whole may be paid on the inventory require d

to be recorded in the Sheriff Court ; or inventory

duty may be paid on the personal property situated

in Scotland, including heritable securities made mov-

able by the Act 31 and 32 Vict. c. 101, § 117, and

duty may be paid on a ''special inventory" of the

heritable securities excluding executors and personal

bonds excluding executors, and probate or adminis-

tration may be obtained in England and Ireland in

respect of the personal estate in these countries, and

duty paid in respect of such on these instruments.

When deceased domiciled furth of the United

Kingdom. — In case of a person dying domiciled furth

of the United Kingdom leaving personal estate in

Scotland, England, and Ireland, an inventory must

be given up in Scotland, probate or administration

taken out in England and Ireland, and duty paid on

such in respect of the property in each country.

In exhibiting inventories after 1st June, 1881, the

amount of debts due and owing by the deceased to

persons in the United Kingdom, and funeral expenses,

may be deducted from, the value of the estate, for

the purpose of paying the inventory duty. The

account of such to be delivered with or annexed to

the affidavit to the inventory.

The debts not to include voluntary debts payable

on death or payable under instruments not bona fide

delivered three months before death. The Commis-

sioners of Inland Revenue within three years may

call for evidence of the contents of or particulars

verified by the affidavit or inventory.

Where the gross estate of a deceased person dying

after 1st June, 1881, docs not exceed £300, and the

estate exceeds £100, if an inventory shall be given

up in accordance with the special provisions of the

Act, the duty to which the inventory is liable is 30s.

— (44 Vict. c. 12, § 34.)

Forms of the inventory and relative affidavit may

be obtained at the Inland Revenue Office (Legacy and

Succession Duty Department).

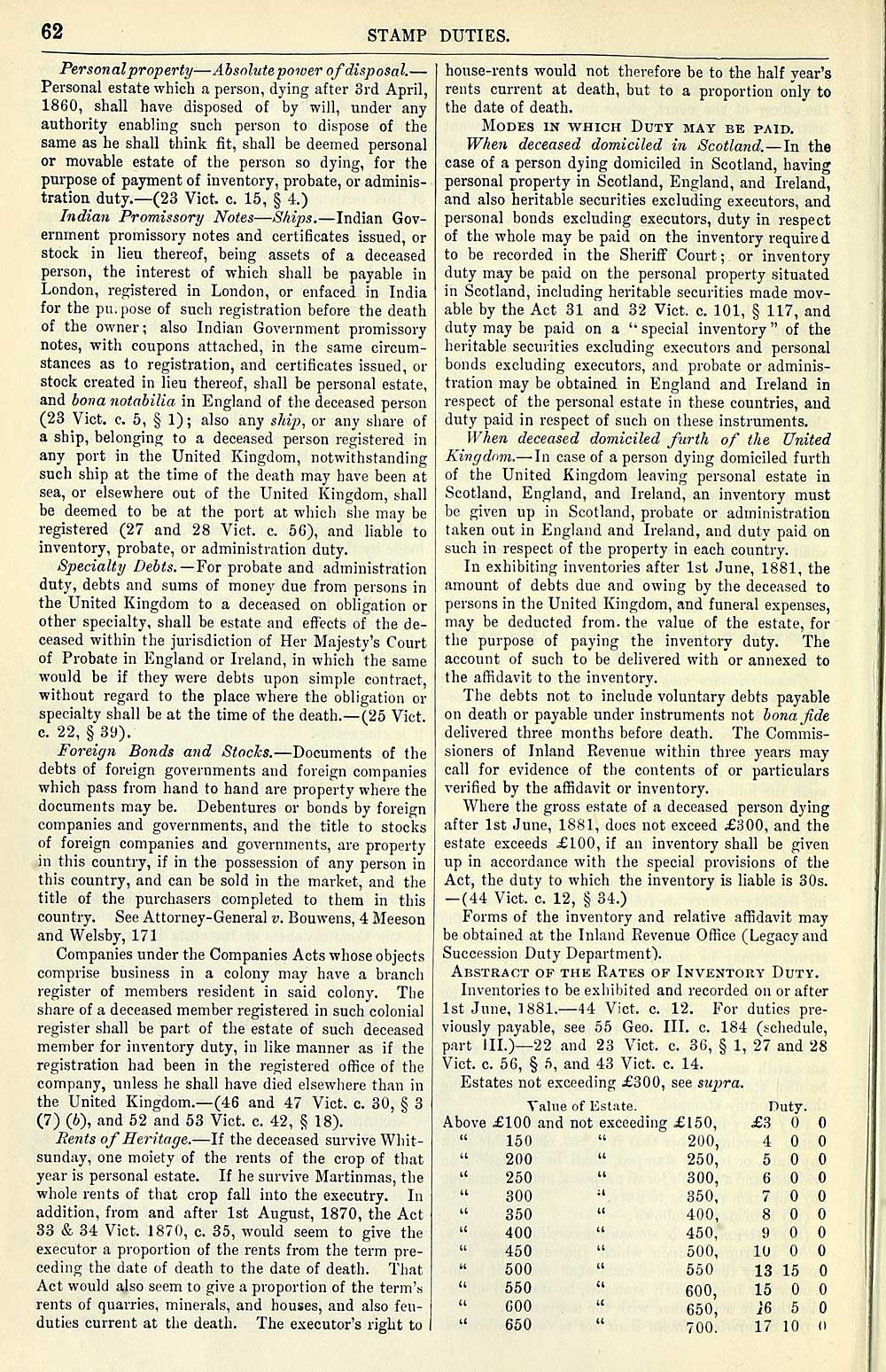

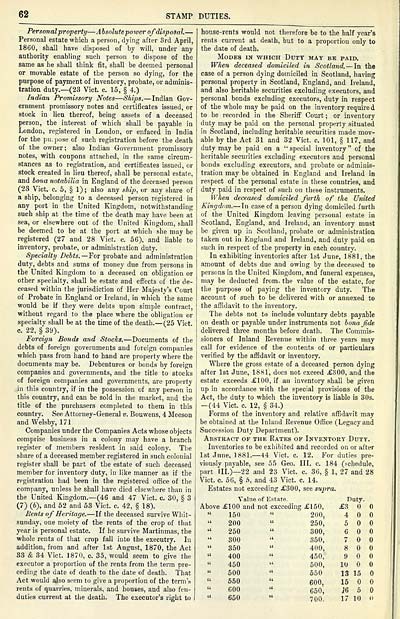

Abstract of thk Rates of Inventory Duty.

Inventories to be exhibited and recorded on or after

1st June, 1881. — 44 Vict. c. 12. For duties pre-

viously payable, see 55 Geo. III. c. 184 (schedule,

part III.)— 22 .and 23 Vict. c. 36, § 1, 27 and 28

Vict. c. 56, § 5, and 43 Vict. c. 14.

Estates not exceeding £300, see sujjra.

Value of Est.ite. Duty.

Above £100 and not exceeding £150, £3

" 150 " 200, 4

" 200 " 250, 5

" 250 " 300, 6

" 300 " 350, 7

" 350 " 400, 8

" 400 " 450, 9

450 " 500, 10

" 500 " 550 13 15

" 660 " 600, 15

GOO " 650, i6 5

" 660 " 700. 17 10 (1

STAMP DUTIES.

Personal property — Absolute power of disposal. —

Personal estate which a person, dying after 8rd April,

1860, shall have disposed of by will, under any

authority enabling such person to dispose of the

same as he shall think fit, shall be deemed personal

or movable estate of the person so dying, for the

purpose of payment of inventory, probate, or adminis-

tration duty.— (23 Vict. c. 15, § 4.)

Indian Promissory Notes — Ships. — Indian Gov-

ernment promissory notes and certificates issued, or

stock in lieu thereof, being assets of a deceased

person, the interest of which shall be payable in

London, registered in London, or enfaced in India

for the pn.pose of such registration before the death

of the owner; also Indian Government promissory

notes, with coupons attached, in the same circum-

stances as to registration, and certificates issued, or

stock created in lieu thereof, shall be personal estate,

and bona notabilia in England of the deceased person

(23 Vict. c. 5, § 1); also any sliip, or any share of

a ship, belonging to a deceased person registered in

any port in the United Kingdom, notwithstanding

such ship at the time of the death may have been at

sea, or elsewhere out of the United Kingdom, shall

be deemed to be at the port at which she may be

registered (27 and 28 Viet. c. 66), and liable to

inventory, probate, or administration duty.

Specialty Debts.— For probate and administration

duty, debts and sums of money due from persons in

the United Kingdom to a deceased on obligation or

other specialty, shall be estate and effects of the de-

ceased within the jurisdiction of Her Majesty's Court

of Probate in England or Ireland, in which the same

would be if they were debts upon simple contract,

without regard to the place where the obligation or

specialty shall be at the time of the death. — (25 Vict,

c. 22, § 39).

Foreign Bonds and Stochs. — Documents of the

debts of foreign governments and foreign companies

which pass from hand to hand are property where the

documents may be. Debentures or bonds by foreign

companies and governments, and the title to stocks

of foreign companies and governments, are property

in this country, if in the possession of any person in

this country, and can be sold in the market, and the

title of the purchasers completed to them in this

country. See Attorney-General v. Bouwens, 4 Meeson

and Welsby, 171

Companies under the Companies Acts whose objects

comprise business in a colony may have a branch

register of members resident in said colony. The

share of a deceased member registered in such colonial

register shall be part of the estate of such deceased

member for inventory duty, in like manner as if the

registration had been in the registered office of the

company, unless he shall have died elsewhere than in

the United Kingdom.— (46 and 47 Vict. c. 30, § 3

(7) (b), and 52 and 53 Vict. c. 42, § 18).

Rents of Heritage. — If the deceased survive Whit-

sunday, one moiety of the rents of the crop of that

year is personal estate. If he survive Martinmas, the

whole rents of that crop fall into the executry. In

addition, from and after 1st August, 1870, the Act

33 & 34 Vict. 1870, c. 35, would seem to give the

executor a proportion of the rents from the term pre-

ceding the date of death to the date of death. That

Act would also seem to give a proportion of the term's

rents of quarries, minerals, and houses, and also fen-

duties current at the death. The executor's right to

house-rents would not therefore be to the half year's

rents current at death, but to a proportion only to

the date of death.

Modes in which Dutt may be paid.

When deceased domiciled in Scotland. — In the

case of a person dying domiciled in Scotland, having

personal property in Scotland, England, and Ireland,

and also heritable securities excluding executors, and

personal bonds excluding executors, duty in respect

of the whole may be paid on the inventory require d

to be recorded in the Sheriff Court ; or inventory

duty may be paid on the personal property situated

in Scotland, including heritable securities made mov-

able by the Act 31 and 32 Vict. c. 101, § 117, and

duty may be paid on a ''special inventory" of the

heritable securities excluding executors and personal

bonds excluding executors, and probate or adminis-

tration may be obtained in England and Ireland in

respect of the personal estate in these countries, and

duty paid in respect of such on these instruments.

When deceased domiciled furth of the United

Kingdom. — In case of a person dying domiciled furth

of the United Kingdom leaving personal estate in

Scotland, England, and Ireland, an inventory must

be given up in Scotland, probate or administration

taken out in England and Ireland, and duty paid on

such in respect of the property in each country.

In exhibiting inventories after 1st June, 1881, the

amount of debts due and owing by the deceased to

persons in the United Kingdom, and funeral expenses,

may be deducted from, the value of the estate, for

the purpose of paying the inventory duty. The

account of such to be delivered with or annexed to

the affidavit to the inventory.

The debts not to include voluntary debts payable

on death or payable under instruments not bona fide

delivered three months before death. The Commis-

sioners of Inland Revenue within three years may

call for evidence of the contents of or particulars

verified by the affidavit or inventory.

Where the gross estate of a deceased person dying

after 1st June, 1881, docs not exceed £300, and the

estate exceeds £100, if an inventory shall be given

up in accordance with the special provisions of the

Act, the duty to which the inventory is liable is 30s.

— (44 Vict. c. 12, § 34.)

Forms of the inventory and relative affidavit may

be obtained at the Inland Revenue Office (Legacy and

Succession Duty Department).

Abstract of thk Rates of Inventory Duty.

Inventories to be exhibited and recorded on or after

1st June, 1881. — 44 Vict. c. 12. For duties pre-

viously payable, see 55 Geo. III. c. 184 (schedule,

part III.)— 22 .and 23 Vict. c. 36, § 1, 27 and 28

Vict. c. 56, § 5, and 43 Vict. c. 14.

Estates not exceeding £300, see sujjra.

Value of Est.ite. Duty.

Above £100 and not exceeding £150, £3

" 150 " 200, 4

" 200 " 250, 5

" 250 " 300, 6

" 300 " 350, 7

" 350 " 400, 8

" 400 " 450, 9

450 " 500, 10

" 500 " 550 13 15

" 660 " 600, 15

GOO " 650, i6 5

" 660 " 700. 17 10 (1

Set display mode to: Large image | Transcription

Images and transcriptions on this page, including medium image downloads, may be used under the Creative Commons Attribution 4.0 International Licence unless otherwise stated. ![]()

| Scottish Post Office Directories > Towns > Glasgow > Post-Office annual Glasgow directory > 1894-1895 > (82) |

|---|

| Permanent URL | https://digital.nls.uk/86359022 |

|---|

| Description | Post-Office annual Glasgow directory 1894-1895 |

|---|---|

| Shelfmark | NH.675-676 |

| Additional NLS resources: | |

| Attribution and copyright: |

|

| Description | Glasgow : Printed by J. Graham for the letter-carriers of the Post-Office, 1828-? Imprint and title vary. [Varying forms of title: Glasgow Post-Office directory, Glasgow Post-Office annual directory, Post Office Glasgow annual directory.] |

|---|---|

| Shelfmark | Various |

| Description | Directories of individual Scottish towns and their suburbs. |

|---|

| Description | Around 700 Scottish directories published annually by the Post Office or private publishers between 1773 and 1911. Most of Scotland covered, with a focus on Edinburgh, Glasgow, Dundee and Aberdeen. Most volumes include a general directory (A-Z by surname), street directory (A-Z by street) and trade directory (A-Z by trade). |

|---|