Download files

Complete book:

Individual page:

{kind=link}

Thumbnail gallery: Grid view | List view

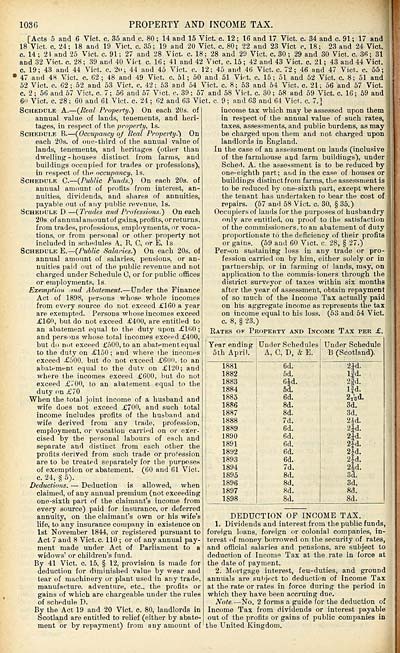

PROPERTY AND INCOME TAX.

12:

1086

[Acts 5 and 6 Vict. c. 35 and c. 80 ; 14 and 15 Vict. c. 12 ; 16 and 17 Vict, c 34 and c. 91 ; 17 and

18 Vict. c. 24; 18 and 19 Vict. c. 35; 19 and 20 Vict. c. 80; 22 and 23 Vict o. 18; 23 and 24 Vict,

c. 14 ; 21 and 25 Vict. c. 91 ; 27 and 28 Vict. c. 18 ; 28 and 29 Vict. c. 30 ; 29 and 30 Viet. c. 3fi ; 31

and 32 Vict. c. 28; 39 and 40 Vict c. 16; 41 and 42 Vict, c. 15; 42 and 43 Vict. c. 21 ; 43 and 44 Vict,

c. 19; 43 and 44 Vict. c. 2(p; 44 and 45 Vict. c. 12; 45 and 46 Vict. c. 72; 46 and 47 Vict. c. 55;

47 and 4« Vict. c. 62; 48 and 49 Vict. c. 61; 50 and 51 Vi^t. c. 15; 51 and 52 Vict. c. 8; 51 and

52 Vict. c. 62; 52 and 53 Vict, c 42; 63 and 54 Vict. c. 8; 63 and 64 Vict. c. 21; 56 and 57 Vict,

c. 2; 56 and 67 Vict. c. 7 ; 56 and 57 Vict. r. 39; 57 and .68 Vict. c. 30; 68 and 69 Vict. c. 16; 69 and

60 Vict. c. 28; 60 and 61 Vict. c. 24 ; 62 and 63 Vict. c. 9 ; and 63 and 64 Vict. c. 7.]

Schedule A. — (^Real Property.} On each 20s. of

annual value of lands, tenements, and heri-

tages, in respect of the property, Is.

Schedule B. — {Occupancy oj Real Property.') On

each 20s. of oue-third of the annual value of

lands, tenements, and heritages (other than

dwelling-houses distinct from farms, and

buildings occupied for trades or professions),

in respect of thn occupancy. Is.

Schedule C. — {Public Funds.) On each 208. of

annual amount of profits from interest, an-

nuities, dividends, and shares of annuities,

payable out of any public revenue, la.

Schedule D — ( Trades and Professions.) On each

20s of annua] aniountof gains, profits, orreturns,

from trades, professions, employments, or voca-

tions, or from personal or other property not

included in schedules A, B, 0, or E, Is

Schedule E. — {Public Salaries.) On each 20s. of

annual amount of salaries, pensions, or an-

nuities paid out of the public revenue and not

charged under Schedule 0, or for public offices

or employments. Is.

Exemption ind Abatement. — Under the Finance

Act of 1898, persons whose whole incomes

from every source do not exceed £160 a year

are exempted. Persons whose incomes exceed

£160, but do not exceed £400, are entitled to

an abatement equal to the duty upon £160 ;

and persons whose total incomes exceed £400,

but do not exceed £500, to an abatement equal

to the duty on £150; und where ihe incomes

exceed £600, but do not exceed £60(i, to an

abatement, equal to the dutv on £120; and

where the incomes exceed £600, but do not

exceed £700, to an abatement equal to the

duty on £70

When the total joint income of a husband and

wife does not excetid £700, and such total

income includes profits of the husband and

wife derived from any trade, profession,

employment, or vocation carried on or exer-

cised by the personal labours of each and

separate and distinct from each other the

profits derived from such trade or profession

are to be treated separately for the purposes

of exemption or abatement. (60 and 61 Vict.

0. 24, § 6).

Deductions. — Deduction is allowed, when

claimed, of any annual premium (not exceeding

one-sixth part of the claimant's income from

every source) paid for insurance, or deferred

annuity, on the claimant's own or his wife's

life, to any insurance company in existence on

1st November 1844, or registered pm'suant to

Act 7 and 8 Vict. c. 110 ; or of any annual pay-

ment made under Act of Parliament to a

widows' or children's fund.

By 41 Vict. c. 16, § 12, provision is made for

deduction for diminished value by wear and

tear of machinery or plant used in any trade,

manufacture, adventure, etc., the profits or

gains of which are chargeable under the rules

of schedule D.

By the Act 19 and 20 Vict. c. 80, landlords in

Scotland are entitled to relief (either by abate-

ment or by repayment) from any amount of

income tax which may be assessed upon them

in respect of the annual value of such rates,

taxes, asses.^ments, and public burdens, as may

be charged upon them and not charged upon

landlords in England.

In the case of an assessment on lands (inclusive

of the farmhouse ai;id farm buildings), under

Sched. A. the assessment is to be reduced by

one-eighth part; aiid in the case of houses or

buildings distinct from farms, the assessment is

to be reduced by one-sixth part, except where

the tenant has undertaken to bear the cost of

repairs. (67 and 58 Vict. c. 30, § 35.)

Occupiers of lands for the purposes of husbandry

only are entitled, on proof to the satisfaction

of the commissioners, to an abatement of duty

proportionate to the deficiency of their profits

or gains. (59 and 60 Vict. c. 28, § 27.)

Person sustaining loss in any trade or pro-

fession carried on by him, either solely or in

partnership, or in farming of lands, may, on

application to the commissioners through the

district surveyor of taxes within six months

after the year of assessment, obtain repayment

of so much of the Income Tax actually paid

on his aggi-egate income as represents the tax

on income equal to his loss. (63 and 54 Vict,

c. 8, § 23.)

Kates of Property and Income Tax per £.

Tear ending

Under Schedules

Under Schedule

5th April.

A, C, D, & E.

B (Scotland).

1881

6d.

21d.

lid.

2|d.

l|d.

1882

5d.

1883

Gid.

1884

5d.

1885

6d.

2iVd.

1886

8d.

3d.

1887

8d.

3d.

1888

7d.

2id.

1889

6d.

2ld.

1890

6d.

2id.

1891

6d.

2id.

1892

6d.

2id.

1893

6d.

2id.

1894

7d.

2id.

1895

8d.

3d.

1896

8d.

3d.

1897

8d.

8d.

1898

8d.

8d.

DEDUCTION OF INCOME TAX.

1. Dividends and interest from the public funds,

foreign loans, foreign or colonial companies, in-

terest nf money borrowed on the security of rates,

and official salaries and pensions, are subject to

deduction of Income Tax at the rate in force at

the date of payment.

2. Mortgage interest, feu-duties, and ground

annuals are sutvject to deduction of Income Tax

at the rate or rates in force during the period in

which they have been accruing due.

Note. — No. 2 forms a guide for the deduction of

Income Tax from dividends or interest payable

out of the profits or gains of public companies in

the United Kingdom.

12:

1086

[Acts 5 and 6 Vict. c. 35 and c. 80 ; 14 and 15 Vict. c. 12 ; 16 and 17 Vict, c 34 and c. 91 ; 17 and

18 Vict. c. 24; 18 and 19 Vict. c. 35; 19 and 20 Vict. c. 80; 22 and 23 Vict o. 18; 23 and 24 Vict,

c. 14 ; 21 and 25 Vict. c. 91 ; 27 and 28 Vict. c. 18 ; 28 and 29 Vict. c. 30 ; 29 and 30 Viet. c. 3fi ; 31

and 32 Vict. c. 28; 39 and 40 Vict c. 16; 41 and 42 Vict, c. 15; 42 and 43 Vict. c. 21 ; 43 and 44 Vict,

c. 19; 43 and 44 Vict. c. 2(p; 44 and 45 Vict. c. 12; 45 and 46 Vict. c. 72; 46 and 47 Vict. c. 55;

47 and 4« Vict. c. 62; 48 and 49 Vict. c. 61; 50 and 51 Vi^t. c. 15; 51 and 52 Vict. c. 8; 51 and

52 Vict. c. 62; 52 and 53 Vict, c 42; 63 and 54 Vict. c. 8; 63 and 64 Vict. c. 21; 56 and 57 Vict,

c. 2; 56 and 67 Vict. c. 7 ; 56 and 57 Vict. r. 39; 57 and .68 Vict. c. 30; 68 and 69 Vict. c. 16; 69 and

60 Vict. c. 28; 60 and 61 Vict. c. 24 ; 62 and 63 Vict. c. 9 ; and 63 and 64 Vict. c. 7.]

Schedule A. — (^Real Property.} On each 20s. of

annual value of lands, tenements, and heri-

tages, in respect of the property, Is.

Schedule B. — {Occupancy oj Real Property.') On

each 20s. of oue-third of the annual value of

lands, tenements, and heritages (other than

dwelling-houses distinct from farms, and

buildings occupied for trades or professions),

in respect of thn occupancy. Is.

Schedule C. — {Public Funds.) On each 208. of

annual amount of profits from interest, an-

nuities, dividends, and shares of annuities,

payable out of any public revenue, la.

Schedule D — ( Trades and Professions.) On each

20s of annua] aniountof gains, profits, orreturns,

from trades, professions, employments, or voca-

tions, or from personal or other property not

included in schedules A, B, 0, or E, Is

Schedule E. — {Public Salaries.) On each 20s. of

annual amount of salaries, pensions, or an-

nuities paid out of the public revenue and not

charged under Schedule 0, or for public offices

or employments. Is.

Exemption ind Abatement. — Under the Finance

Act of 1898, persons whose whole incomes

from every source do not exceed £160 a year

are exempted. Persons whose incomes exceed

£160, but do not exceed £400, are entitled to

an abatement equal to the duty upon £160 ;

and persons whose total incomes exceed £400,

but do not exceed £500, to an abatement equal

to the duty on £150; und where ihe incomes

exceed £600, but do not exceed £60(i, to an

abatement, equal to the dutv on £120; and

where the incomes exceed £600, but do not

exceed £700, to an abatement equal to the

duty on £70

When the total joint income of a husband and

wife does not excetid £700, and such total

income includes profits of the husband and

wife derived from any trade, profession,

employment, or vocation carried on or exer-

cised by the personal labours of each and

separate and distinct from each other the

profits derived from such trade or profession

are to be treated separately for the purposes

of exemption or abatement. (60 and 61 Vict.

0. 24, § 6).

Deductions. — Deduction is allowed, when

claimed, of any annual premium (not exceeding

one-sixth part of the claimant's income from

every source) paid for insurance, or deferred

annuity, on the claimant's own or his wife's

life, to any insurance company in existence on

1st November 1844, or registered pm'suant to

Act 7 and 8 Vict. c. 110 ; or of any annual pay-

ment made under Act of Parliament to a

widows' or children's fund.

By 41 Vict. c. 16, § 12, provision is made for

deduction for diminished value by wear and

tear of machinery or plant used in any trade,

manufacture, adventure, etc., the profits or

gains of which are chargeable under the rules

of schedule D.

By the Act 19 and 20 Vict. c. 80, landlords in

Scotland are entitled to relief (either by abate-

ment or by repayment) from any amount of

income tax which may be assessed upon them

in respect of the annual value of such rates,

taxes, asses.^ments, and public burdens, as may

be charged upon them and not charged upon

landlords in England.

In the case of an assessment on lands (inclusive

of the farmhouse ai;id farm buildings), under

Sched. A. the assessment is to be reduced by

one-eighth part; aiid in the case of houses or

buildings distinct from farms, the assessment is

to be reduced by one-sixth part, except where

the tenant has undertaken to bear the cost of

repairs. (67 and 58 Vict. c. 30, § 35.)

Occupiers of lands for the purposes of husbandry

only are entitled, on proof to the satisfaction

of the commissioners, to an abatement of duty

proportionate to the deficiency of their profits

or gains. (59 and 60 Vict. c. 28, § 27.)

Person sustaining loss in any trade or pro-

fession carried on by him, either solely or in

partnership, or in farming of lands, may, on

application to the commissioners through the

district surveyor of taxes within six months

after the year of assessment, obtain repayment

of so much of the Income Tax actually paid

on his aggi-egate income as represents the tax

on income equal to his loss. (63 and 54 Vict,

c. 8, § 23.)

Kates of Property and Income Tax per £.

Tear ending

Under Schedules

Under Schedule

5th April.

A, C, D, & E.

B (Scotland).

1881

6d.

21d.

lid.

2|d.

l|d.

1882

5d.

1883

Gid.

1884

5d.

1885

6d.

2iVd.

1886

8d.

3d.

1887

8d.

3d.

1888

7d.

2id.

1889

6d.

2ld.

1890

6d.

2id.

1891

6d.

2id.

1892

6d.

2id.

1893

6d.

2id.

1894

7d.

2id.

1895

8d.

3d.

1896

8d.

3d.

1897

8d.

8d.

1898

8d.

8d.

DEDUCTION OF INCOME TAX.

1. Dividends and interest from the public funds,

foreign loans, foreign or colonial companies, in-

terest nf money borrowed on the security of rates,

and official salaries and pensions, are subject to

deduction of Income Tax at the rate in force at

the date of payment.

2. Mortgage interest, feu-duties, and ground

annuals are sutvject to deduction of Income Tax

at the rate or rates in force during the period in

which they have been accruing due.

Note. — No. 2 forms a guide for the deduction of

Income Tax from dividends or interest payable

out of the profits or gains of public companies in

the United Kingdom.

Set display mode to: Large image | Transcription

Images and transcriptions on this page, including medium image downloads, may be used under the Creative Commons Attribution 4.0 International Licence unless otherwise stated. ![]()

| Scottish Post Office Directories > Towns > Edinburgh > Post Office Edinburgh and Leith directory > 1900-1901 > (1106) |

|---|

| Permanent URL | https://digital.nls.uk/85357106 |

|---|

| Description | Post-Office Edinburgh & Leith directory 1900-01 |

|---|---|

| Shelfmark | POE |

| Additional NLS resources: | |

| Attribution and copyright: |

|

| Description | Edinburgh : Postmaster General, [1846-1975]. Preceded by: Edinburgh & Leith Post Office Directory Limited. |

|---|---|

| Shelfmark | Various |

| Description | Directories of individual Scottish towns and their suburbs. |

|---|

| Description | Around 700 Scottish directories published annually by the Post Office or private publishers between 1773 and 1911. Most of Scotland covered, with a focus on Edinburgh, Glasgow, Dundee and Aberdeen. Most volumes include a general directory (A-Z by surname), street directory (A-Z by street) and trade directory (A-Z by trade). |

|---|