Download files

Complete book:

Individual page:

{kind=link}

Thumbnail gallery: Grid view | List view

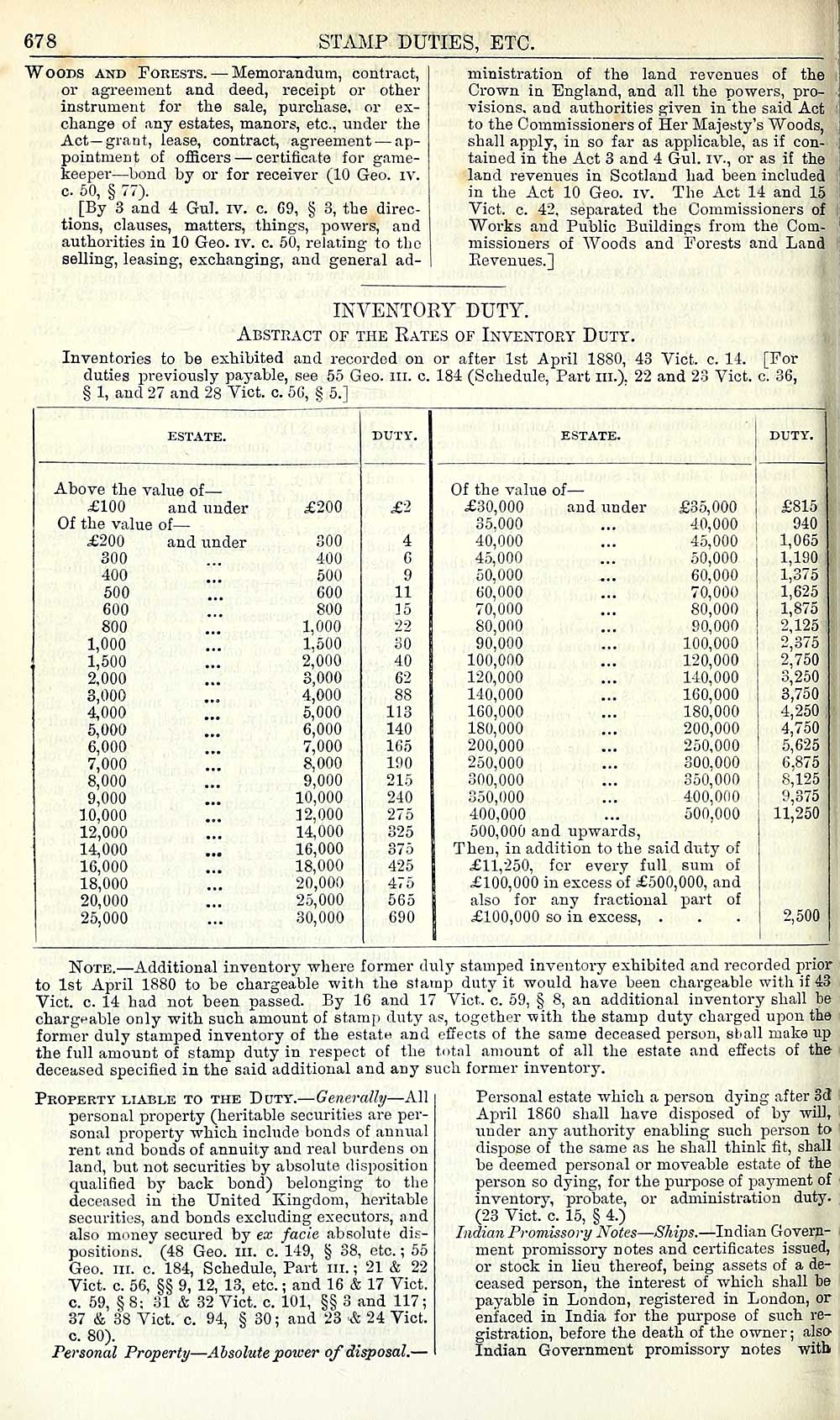

678

STAMP DUTIES, ETC.

Woods and Forests. — Memorandum, contract,

or agreement and deed, receipt or other

instrument for the sale, purchase, or ex-

change of any estates, manors, etc., under the

Act— grant, lease, contract, agreement — ap-

pointment of officers — certificate for game-

keeper — bond by or for receiver (10 Geo. IV.

c 50, § 77).

_ [By 3 and 4 Gul. iv. c. 69, § 3, the direc-

tions, clauses, matters, things, powers, and

authorities in 10 Geo. iv. c. 50, relating to the

selling, leasing, exchanging, and general ad-

ministration of the land revenues of the

Crown in England, and all the powers, pro-

visions, and authorities given in the said Act :

to the Commissioners of Her Majesty's Woods,

shall apply, in so far as applicable, as if con-

tained in the Act 3 and 4 Gul. iv., or as if the

land revenues in Scotland had been included

in the Act 10 Geo. iv. The Act 14 and 15

Vict. c. 42, separated the Commissioners of

Works and Public Buildings from the Com-

missioners of Woods and Forests and Land

Eevenues.]

INVENTORY DUTY.

Abstract of the Rates of Inventory Duty.

Inventories to be exhibited and recorded on or after 1st April 1880, 43 Vict. c. 14. [For

duties previously payable, see 55 Geo. in. c. 184 (Schedule, Part in.). 22 and 23 Vict. c. 36,

§ 1, and 27 and 28 Vict. c. 56, § 5.]

ESTATE.

DUTY.

ESTATE.

DUTY.

Above the value of —

Of the value of —

£100 and under

£200

£2

£30,000 and under

£35,000

£815

Of the value of —

35.000

40,000

940

£200 and under

300

4

40,000

45,000

1,065

300

400

6

45,000

50,000

1,190

400

500

9

50,000

60,000

1,375

500

600

11

60,000

70,000

1,625

600

800

15

70,000

80,000

1,875

800

1,000

22

80,000

90,000

2,125

1,000

1.500

30

90,000

100,000

2,375

1,500

2,000

40

100,000

120,000

2,750

2,000

3,000

62

120,000

140,000

3,250

3,000

4,000

88

140,000

160,000

3,750

4,000

5,000

113

160,000

180,000

4,250 ;

5,000

6,000

140

180,000

200,000

4,750

6,000

7,000

165

200,000

250,000

5,625

7,000

8,000

190

250,000

300,000

6,875

8,000

9,000

215

300,000

350,000

8,125

9,000

10,000

240

350,000

400,000

9,375

10,000

12,000

275

400,000

500,000

11,250

12,000

14,000

325

500,000 and upwards,

14,000

16,000

375

Then, in addition to the sai

1 duty of

16,000

18,000

425

£11,250, for every full

sum of

18,000

20,000

475

£100,000 in excess of £500,000, and

20,000

25,000

565

also for any fractional

part of

25,000

30,000

690

£100,000 so in excess, .

2,500

Note. — Additional inventory where former duly stamped inventory exhibited and recorded prior

to 1st April 1880 to be chargeable with the stamp duty it would have been chargeable with if 43

Vict. c. 14 had not been passed. By 16 and 17 Vict. c. 59, § 8, an additional inventory shall be

chargeable only with such amount of stamp duty as, together with the stamp duty charged upon the

former duly stamped inventory of the estate and effects of the same deceased person, shall make up

the full amount of stamp duty in respect of the total amount of all the estate and effects of the

deceased specified in the said additional and any such former inventory.

Property liable to the Duty. — Generally — All

personal property (heritable securities are per-

sonal property which include bonds of annual

rent and bonds of annuity and real burdens on

land, but not securities by absolute disposition

qualified by back bond) belonging to the

deceased in the United Kingdom, heritable

securities, and bonds excluding executors, and

also money secured by ex facie absolute dis-

positions. (48 Geo. in. c. 149, § 38, etc. ; 55

Geo. in. c. 184, Schedule, Part in. ; 21 & 22

Vict. c. 56, §§ 9, 12, 13, etc. ; and 16 & 17 Vict.

c. 59, § 8: 31 & 32 Vict. c. 101, §§ 3 and 117;

37 & 38 Vict. c. 94, § 30; and 23 & 24 Vict.

c. 80).

Personal Property — Absolute power of disposal. —

Personal estate which a person dying after 36!

April 1860 shall have disposed of by will,

under any authority enabling such person to

dispose of the same as he shall think fit, shall

be deemed personal or moveable estate of the

person so dying, for the purpose of payment of

inventory, probate, or administration duty.

(23 Vict. c. 15, § 4.)

Indian Promissory Notes — Ships. — Indian Govern-

ment promissory notes and certificates issued,

or stock in lieu thereof, being assets of a de-

ceased person, the interest of which shall be

payable in London, registered in London, or

enfaced in India for the purpose of such re-

gistration, before the death of the owner ; also-

Indian Government promissory notes with

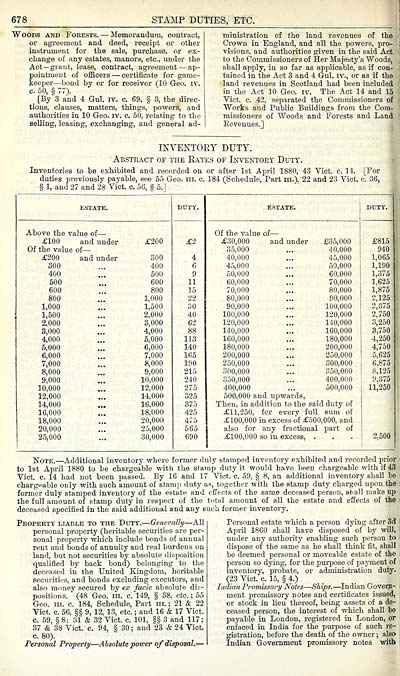

STAMP DUTIES, ETC.

Woods and Forests. — Memorandum, contract,

or agreement and deed, receipt or other

instrument for the sale, purchase, or ex-

change of any estates, manors, etc., under the

Act— grant, lease, contract, agreement — ap-

pointment of officers — certificate for game-

keeper — bond by or for receiver (10 Geo. IV.

c 50, § 77).

_ [By 3 and 4 Gul. iv. c. 69, § 3, the direc-

tions, clauses, matters, things, powers, and

authorities in 10 Geo. iv. c. 50, relating to the

selling, leasing, exchanging, and general ad-

ministration of the land revenues of the

Crown in England, and all the powers, pro-

visions, and authorities given in the said Act :

to the Commissioners of Her Majesty's Woods,

shall apply, in so far as applicable, as if con-

tained in the Act 3 and 4 Gul. iv., or as if the

land revenues in Scotland had been included

in the Act 10 Geo. iv. The Act 14 and 15

Vict. c. 42, separated the Commissioners of

Works and Public Buildings from the Com-

missioners of Woods and Forests and Land

Eevenues.]

INVENTORY DUTY.

Abstract of the Rates of Inventory Duty.

Inventories to be exhibited and recorded on or after 1st April 1880, 43 Vict. c. 14. [For

duties previously payable, see 55 Geo. in. c. 184 (Schedule, Part in.). 22 and 23 Vict. c. 36,

§ 1, and 27 and 28 Vict. c. 56, § 5.]

ESTATE.

DUTY.

ESTATE.

DUTY.

Above the value of —

Of the value of —

£100 and under

£200

£2

£30,000 and under

£35,000

£815

Of the value of —

35.000

40,000

940

£200 and under

300

4

40,000

45,000

1,065

300

400

6

45,000

50,000

1,190

400

500

9

50,000

60,000

1,375

500

600

11

60,000

70,000

1,625

600

800

15

70,000

80,000

1,875

800

1,000

22

80,000

90,000

2,125

1,000

1.500

30

90,000

100,000

2,375

1,500

2,000

40

100,000

120,000

2,750

2,000

3,000

62

120,000

140,000

3,250

3,000

4,000

88

140,000

160,000

3,750

4,000

5,000

113

160,000

180,000

4,250 ;

5,000

6,000

140

180,000

200,000

4,750

6,000

7,000

165

200,000

250,000

5,625

7,000

8,000

190

250,000

300,000

6,875

8,000

9,000

215

300,000

350,000

8,125

9,000

10,000

240

350,000

400,000

9,375

10,000

12,000

275

400,000

500,000

11,250

12,000

14,000

325

500,000 and upwards,

14,000

16,000

375

Then, in addition to the sai

1 duty of

16,000

18,000

425

£11,250, for every full

sum of

18,000

20,000

475

£100,000 in excess of £500,000, and

20,000

25,000

565

also for any fractional

part of

25,000

30,000

690

£100,000 so in excess, .

2,500

Note. — Additional inventory where former duly stamped inventory exhibited and recorded prior

to 1st April 1880 to be chargeable with the stamp duty it would have been chargeable with if 43

Vict. c. 14 had not been passed. By 16 and 17 Vict. c. 59, § 8, an additional inventory shall be

chargeable only with such amount of stamp duty as, together with the stamp duty charged upon the

former duly stamped inventory of the estate and effects of the same deceased person, shall make up

the full amount of stamp duty in respect of the total amount of all the estate and effects of the

deceased specified in the said additional and any such former inventory.

Property liable to the Duty. — Generally — All

personal property (heritable securities are per-

sonal property which include bonds of annual

rent and bonds of annuity and real burdens on

land, but not securities by absolute disposition

qualified by back bond) belonging to the

deceased in the United Kingdom, heritable

securities, and bonds excluding executors, and

also money secured by ex facie absolute dis-

positions. (48 Geo. in. c. 149, § 38, etc. ; 55

Geo. in. c. 184, Schedule, Part in. ; 21 & 22

Vict. c. 56, §§ 9, 12, 13, etc. ; and 16 & 17 Vict.

c. 59, § 8: 31 & 32 Vict. c. 101, §§ 3 and 117;

37 & 38 Vict. c. 94, § 30; and 23 & 24 Vict.

c. 80).

Personal Property — Absolute power of disposal. —

Personal estate which a person dying after 36!

April 1860 shall have disposed of by will,

under any authority enabling such person to

dispose of the same as he shall think fit, shall

be deemed personal or moveable estate of the

person so dying, for the purpose of payment of

inventory, probate, or administration duty.

(23 Vict. c. 15, § 4.)

Indian Promissory Notes — Ships. — Indian Govern-

ment promissory notes and certificates issued,

or stock in lieu thereof, being assets of a de-

ceased person, the interest of which shall be

payable in London, registered in London, or

enfaced in India for the purpose of such re-

gistration, before the death of the owner ; also-

Indian Government promissory notes with

Set display mode to: Large image | Transcription

Images and transcriptions on this page, including medium image downloads, may be used under the Creative Commons Attribution 4.0 International Licence unless otherwise stated. ![]()

| Scottish Post Office Directories > Towns > Edinburgh > Post Office Edinburgh and Leith directory > 1880-1881 > (720) |

|---|

| Permanent URL | https://digital.nls.uk/84275917 |

|---|

| Description | Post-Office Edinburgh & Leith directory 1880-81 |

|---|---|

| Shelfmark | POE |

| Additional NLS resources: | |

| Attribution and copyright: |

|

| Description | Edinburgh : Postmaster General, [1846-1975]. Preceded by: Edinburgh & Leith Post Office Directory Limited. |

|---|---|

| Shelfmark | Various |

| Description | Directories of individual Scottish towns and their suburbs. |

|---|

| Description | Around 700 Scottish directories published annually by the Post Office or private publishers between 1773 and 1911. Most of Scotland covered, with a focus on Edinburgh, Glasgow, Dundee and Aberdeen. Most volumes include a general directory (A-Z by surname), street directory (A-Z by street) and trade directory (A-Z by trade). |

|---|