Download files

Complete book:

Individual page:

Thumbnail gallery: Grid view | List view

2

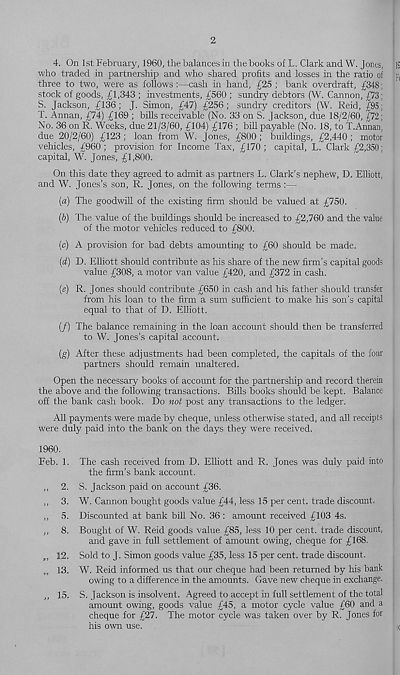

4. On 1st February, 1960, the balances in the books of L. Clark and W. Jones,

who traded in partnership and who shared profits and losses in the ratio of

three to two, were as follows :—cash in hand, £25 ; bank overdraft, £348;

stock of goods, £1,343 ; investments, £560 ; sundry debtors (W. Cannon, £73;

S. Jackson, £136; J. Simon, £47) £256; sundry creditors (W. Reid, £95;

T. Annan, £74) £169 ; bills receivable (No. 33 on S. Jackson, due 18/2/60, £72;

No. 36 on R. Weeks, due 21/3/60, £104) £176 ; bill payable (No. 18, to T.Annan,

due 20/2/60) £123 ; loan from W. Jones, £800 ; buildings, £2,440 ; motor

vehicles, £960; provision for Income Tax, £170; capital, L. Clark £2,350;

capital, W. Jones, £1,800.

On this date they agreed to admit as partners L. Clark’s nephew, D. Elliott,

and W. Jones’s son, R. Jones, on the following terms :—

(a) The goodwill of the existing firm should be valued at £750.

(b) The value of the buildings should be increased to £2,760 and the value

of the motor vehicles reduced to £800.

(c) A provision for bad debts amounting to £60 should be made.

(d) D. Elliott should contribute as his share of the new firm’s capital goods

value £308, a motor van value £420, and £372 in cash.

(e) R. Jones should contribute £650 in cash and his father should transfer

from his loan to the firm a sum sufficient to make his son’s capital

equal to that of D. Elliott.

(/) The balance remaining in the loan account should then be transferred

to W. Jones’s capital account.

(g) After these adjustments had been completed, the capitals of the four

partners should remain unaltered.

Open the necessary books of account for the partnership and record therein

the above and the following transactions. Bills books should be kept. Balance

off the bank cash book. Do not post any transactions to the ledger.

All payments were made by cheque, unless otherwise stated, and all receipts

were duly paid into the bank on the days they were received.

1960.

Feb. 1. The cash received from D. Elliott and R. Jones was duly paid into

the firm’s bank account.

,, 2. S. Jackson paid on account £36.

,, 3. W. Cannon bought goods value £44, less 15 per cent, trade discount.

,, 5. Discounted at bank bill No. 36 : amount received £103 4s.

,, 8. Bought of W. Reid goods value £85, less 10 per cent, trade discount,

and gave in full settlement of amount owing, cheque for £168.

„ 12. Sold to J. Simon goods value £35, less 15 per cent, trade discount.

„ 13. W. Reid informed us that our cheque had been returned by his bank

owing to a difference in the amounts. Gave new cheque in exchange.

,, 15. S. Jackson is insolvent. Agreed to accept in full settlement of the total

amount owing, goods value £45, a motor cycle value £60 and a

cheque for £27. The motor cycle was taken over by R. Jones for

his own use.

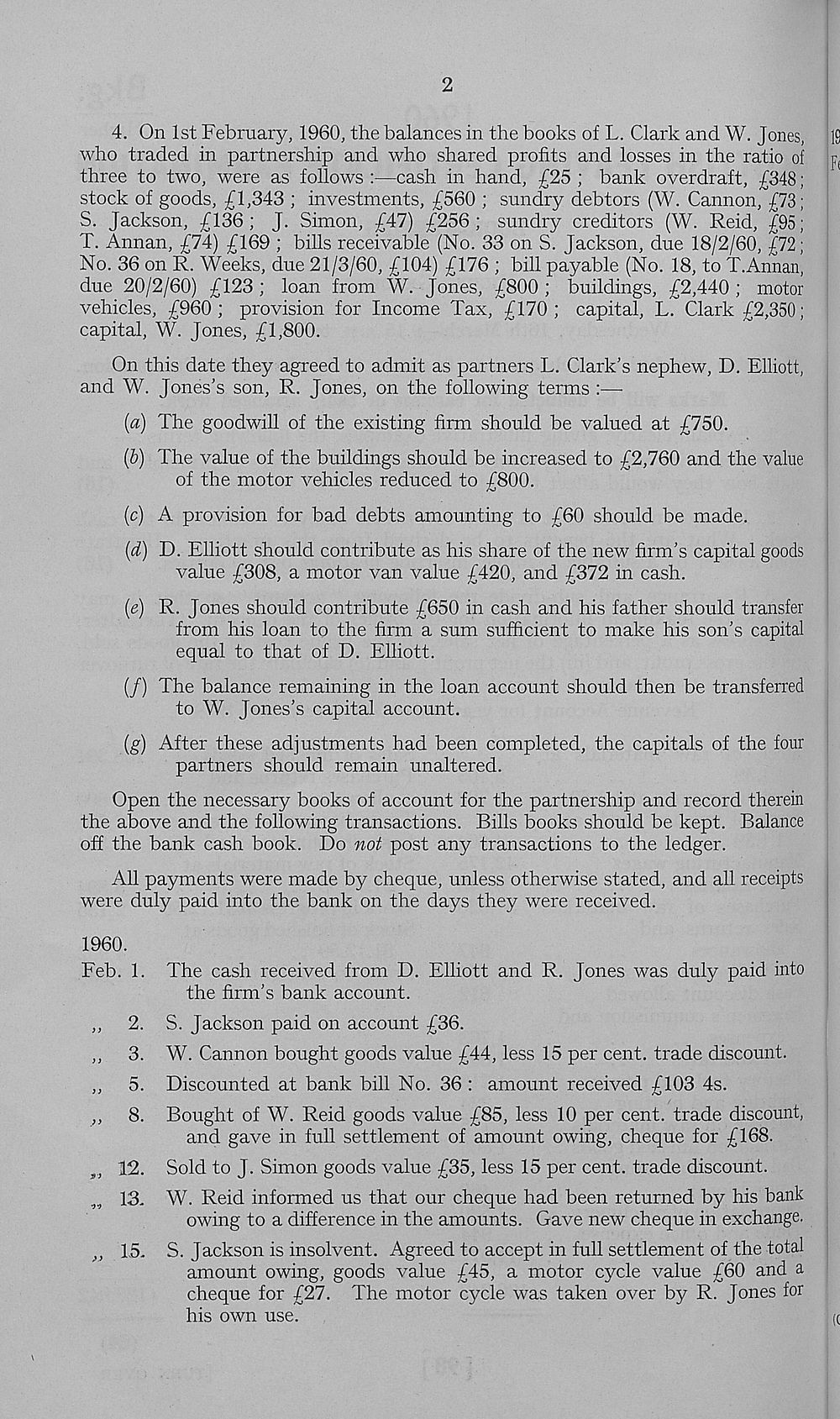

4. On 1st February, 1960, the balances in the books of L. Clark and W. Jones,

who traded in partnership and who shared profits and losses in the ratio of

three to two, were as follows :—cash in hand, £25 ; bank overdraft, £348;

stock of goods, £1,343 ; investments, £560 ; sundry debtors (W. Cannon, £73;

S. Jackson, £136; J. Simon, £47) £256; sundry creditors (W. Reid, £95;

T. Annan, £74) £169 ; bills receivable (No. 33 on S. Jackson, due 18/2/60, £72;

No. 36 on R. Weeks, due 21/3/60, £104) £176 ; bill payable (No. 18, to T.Annan,

due 20/2/60) £123 ; loan from W. Jones, £800 ; buildings, £2,440 ; motor

vehicles, £960; provision for Income Tax, £170; capital, L. Clark £2,350;

capital, W. Jones, £1,800.

On this date they agreed to admit as partners L. Clark’s nephew, D. Elliott,

and W. Jones’s son, R. Jones, on the following terms :—

(a) The goodwill of the existing firm should be valued at £750.

(b) The value of the buildings should be increased to £2,760 and the value

of the motor vehicles reduced to £800.

(c) A provision for bad debts amounting to £60 should be made.

(d) D. Elliott should contribute as his share of the new firm’s capital goods

value £308, a motor van value £420, and £372 in cash.

(e) R. Jones should contribute £650 in cash and his father should transfer

from his loan to the firm a sum sufficient to make his son’s capital

equal to that of D. Elliott.

(/) The balance remaining in the loan account should then be transferred

to W. Jones’s capital account.

(g) After these adjustments had been completed, the capitals of the four

partners should remain unaltered.

Open the necessary books of account for the partnership and record therein

the above and the following transactions. Bills books should be kept. Balance

off the bank cash book. Do not post any transactions to the ledger.

All payments were made by cheque, unless otherwise stated, and all receipts

were duly paid into the bank on the days they were received.

1960.

Feb. 1. The cash received from D. Elliott and R. Jones was duly paid into

the firm’s bank account.

,, 2. S. Jackson paid on account £36.

,, 3. W. Cannon bought goods value £44, less 15 per cent, trade discount.

,, 5. Discounted at bank bill No. 36 : amount received £103 4s.

,, 8. Bought of W. Reid goods value £85, less 10 per cent, trade discount,

and gave in full settlement of amount owing, cheque for £168.

„ 12. Sold to J. Simon goods value £35, less 15 per cent, trade discount.

„ 13. W. Reid informed us that our cheque had been returned by his bank

owing to a difference in the amounts. Gave new cheque in exchange.

,, 15. S. Jackson is insolvent. Agreed to accept in full settlement of the total

amount owing, goods value £45, a motor cycle value £60 and a

cheque for £27. The motor cycle was taken over by R. Jones for

his own use.

Set display mode to:

![]() Universal Viewer |

Universal Viewer | ![]() Mirador |

Large image | Transcription

Mirador |

Large image | Transcription

Images and transcriptions on this page, including medium image downloads, may be used under the Creative Commons Attribution 4.0 International Licence unless otherwise stated. ![]()

| Scottish school exams and circulars > Scottish Leaving Certificate Examination > 1960 > (354) |

|---|

| Permanent URL | https://digital.nls.uk/130091300 |

|---|

| Attribution and copyright: |

|

|---|---|

| Shelfmark | GEB.16 |

|---|---|

| Additional NLS resources: | |

| Description | Examination papers for the School Leaving Certificate 1888-1961 and the Scottish Certificate of Education 1962-1963. Produced by the Scotch (later 'Scottish') Education Department, these exam papers show how education developed in Scotland over this period, with a growing choice of subjects. Comparing them with current exam papers, there are obvious differences in the content and standards of the questions, and also in the layout and use of language |

|---|---|

| Additional NLS resources: |

|

{kind=link}